Retirement Taxes: These 6 Sources of Retirement Income Are Not Taxable

One often-overlooked aspect of retirement planning is the effect of taxes. Without proper planning, taxes can take a significant bite out of your nest egg.

Zelle Scams on Facebook Marketplace: How To Recognize and Avoid Them

Growing Up Poor: 13 Ways You’re Taught To Never Waste Money

A $1 million dollar portfolio in a 401(k) plan or traditional IRA, for example, might be worth $800,000 or less after taxes. Similarly, if your investments are in a regular, taxable brokerage account, the income that money generates may also be taxable.

One way to work around this problem is to save and invest even more during your working years so that you have extra money to pay your taxes. Another is to be tax-smart with your investments and account choices to reduce your tax liability to an absolute minimum. While many things are surprisingly taxed in retirement, here are several types of retirement income that are not taxable.

Roth Withdrawals

The easiest way to avoid taxes on your retirement money is to use a Roth account. Both IRA and 401(k) plans can be structured as Roth accounts, which don’t offer a tax deduction on contributions but allow tax-free withdrawals after age 59 ½.

Essentially, with a Roth account, you’re paying your taxes upfront at the time that you contribute, rather than owing them on your distributions. While you can’t contribute to a Roth if your income exceeds certain levels — $153,000 for singles or $228,000 for joint filers in 2023 — you can convert your traditional plan to a Roth at any time. However, you’ll have to pay income taxes on the amount of the conversion, just as if you withdrew the money.

For this reason, it typically makes more sense to start a Roth earlier in your career rather than facing a huge tax bill during your peak earning years.

Bill Gates: 7 Things He Won’t Waste Money On

How To Go From Broke in Your 40s to Millionaire in Your 50s: 8 ‘Late Start’ Retirement Tips

Inheritances

It’s not usually a good idea to rely on an inheritance as a retirement plan. For starters, receiving an inheritance is never a sure thing, and additionally, the amount bequeathed is rarely enough to fund a long retirement.

However, many Americans do receive an inheritance at some point in their lives, and it can often be a good supplement to existing retirement savings. Financially speaking, the best part of an inheritance is that it is tax-free. Even if there is estate tax involved, which is quite a rarity, beneficiaries are not responsible for paying them.

Downsizing for Retirement? Stay Away From These 7 Homes

Housing Market 2023: The 10 Most Overpriced Housing Markets in the US — 5 Are in Florida

Municipal Bond Income

Municipal bonds are issued by states, cities and various localities, generally to fund projects like schools, roads and other items that are for the common good. Municipal bonds are granted tax relief at the federal level, meaning investors don’t have to pay federal taxes on the interest earned from any municipal bond.

If you buy a bond issued in your own state, you’re typically granted a tax exemption from state taxes, as well. This makes municipal bonds particularly valuable in high-tax states like California. They can also be a good source of retirement income, as they are generally safe investments in addition to being tax-exempt.

HSA Withdrawals

A health savings account (HSA) combines some of the best features of both traditional and Roth IRAs into a single package. Contributions to an HSA earn a tax deduction, and earnings within the account grow tax-free.

When used for qualifying healthcare expenses, which is a fairly broad category, withdrawals are tax-exempt, as well. Otherwise, you’ll face a steep 20% penalty on your withdrawals. However, the kicker in terms of retirement planning is that once you reach age 65, you can withdraw your HSA money for any reason at all without having to pay a penalty.

When used for non-healthcare purposes, you’ll still face ordinary income tax, but you can avoid the penalty. The best use of an HSA will always be for healthcare expenses, though, as you can withdraw your funds tax-free at any time.

Some Social Security Payments

In many cases, Social Security payments are not taxable, but this is not always the case. If you’re simply living off your Social Security retirement benefits, then it’s true that they are tax-free. However, if you earn over a certain amount, some or even most of your payments become taxable. Here’s how the taxation of Social Security for 2022 breaks down, based on income and filing status:

- Individuals with a combined income of $25,000 to $34,000 may have to pay tax on up to 50% of their benefits; those with incomes of over $34,000 may face taxes on up to 85% of their Social Security income.

- For joint filers, up to 50% of Social Security income is taxable for incomes between $32,000 and $44,000, with those earning more paying tax on up to 85% of benefits.

The Social Security Administration defines “combined income” as adjusted gross income plus nontaxable interest plus one-half of Social Security benefits.

I’m a Financial Advisor: Here’s How Often You Should Check Your Retirement Account Balance

Life Insurance Proceeds

Just like an inheritance, waiting for a life insurance payout isn’t an ideal strategy for funding a retirement plan. However, it’s entirely possible that at some point in your senior years, you will receive some type of life insurance payout.

Often, these distributions are in the hundreds-of-thousands-of-dollars range, so they can significantly impact your retirement savings. And just as with inheritances, life insurance proceeds are tax-free to the recipient, at least when taken in a lump sum rather than installments.

More From GOBankingRates

- Housing Market 2023: The 10 Most Overpriced Housing Markets in the US -- 5 Are in Florida

- How To Get Free Money: 13 Proven Ways

- 3 Things You Must Do When Your Savings Reach $50,000

- How To Make a Savings Plan: 6 Steps You Can Take

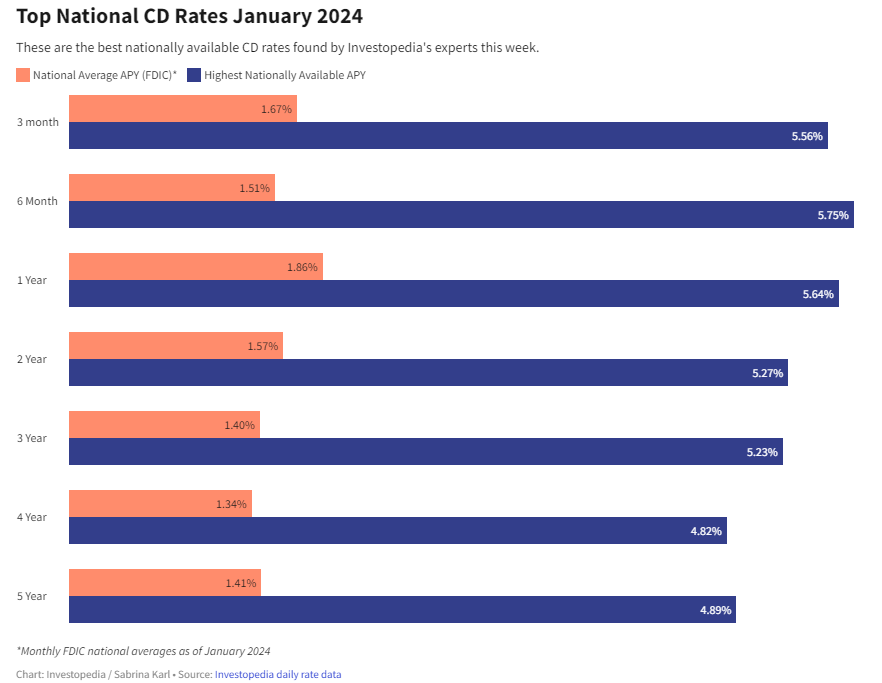

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create

What is the National Debt?

As a professional in the field of finance and economics, it is essential to have a comprehensive understanding of the national debt. The national debt refers to the total amount of money that a country owes to its creditors, which may include individuals, businesses, and other countries. In this art

How to retire in other countries? What are the best countries to retire abroad?

Retiring abroad has become an increasingly popular option for many people seeking a change of pace and a more affordable lifestyle. However, making the decision to retire in another country requires careful consideration and planning. In this article, we will explore the best countries to retire abr