Suze Orman: 3 Moves To Make If You Can Only Save $100 a Month

If you save roughly $600 per month at a 6% return, after 10 years you’d have saved nearly $100,000. But most people, especially in today’s economy, can’t free up $600 per month to build their savings. If you saved just 10% of your income, you’d have to earn $6,000 per month, or $72,000 per year, to save $600.

Find: 5 Things Warren Buffett Says To Do Before a Recession Hits

See Our List: 100 Most Influential Money Experts

For many people, saving $100 per month seems to be a more attainable goal. Once you have allocated that money to save, though, what should you do with it?

Deposit It In a High Yield Online Savings Account

Financial experts like Suze Orman — co-founder of emergency savings startup SecureSave — suggest you focus on building emergency savings as the first step to financial security, even before paying down high-interest credit card debt. “You should absolutely put it in an emergency savings account,” Orman recently told GOBankingRates in an exclusive interview. “Because even if you pay down your credit card debt, you then don’t have any money.”

If something happens that requires $100 quickly, she said, you might be forced to use your credit card to pay for the expense — or, worse, take out a cash advance on your credit card. “Maybe you’ve brought down your debt a little bit… what good did it do for you?” she said.

Instead, putting that money in savings “might make you feel a bit more secure, that you have $100 in savings, which would change your psyche,” Orman indicated.

She pointed out that the goal of money is to help you feel secure. If having $100 cash in the bank will do that, it’s the best way to use that money.

Also: Jaspreet Singh Shares 5 Ways To Grow $10k to $100k in Three Years

Pay Down High Interest Debt

Apart from depositing $100 in a high-yield savings account, Orman has previously shared other ways to put $100 to good use in growing your financial security. Once you’ve built an emergency savings fund that makes you feel at ease — a varying amount depending on your expenses and any safety nets (such as a second job or side gigs) — it’s time to start paying down debt.

In fact, even if you haven’t built enough of a financial buffer in a high-yield savings account, you should do whatever you can to start paying down high-interest debt.

“The last thing you want to have hanging over your head if a recession causes a layoff in your household, or reduced hours, is to have to stay current on a very costly credit card balance,” she wrote in an April 6 blog post. “Please be extra strong right now, and scour your spending to find ways you can reduce your costs, so you have more to put toward paying down high-rate credit card debt.”

Boost Your Retirement Savings

If your credit card debt is minimal and you’re paying off your cards at the end of every month, it’s time to look into long-term investments with any extra cash you have, even if it’s only $100 a month.

“If you have a workplace retirement plan that includes a matching contribution from your employer, that’s the best, first place to save for retirement,” Orman wrote in a separate blog post. “If you aren’t yet saving at least 10% of your income, now is the time to get closer to that target.”

Solidify Your Financial Base

Big changes to your financial future begin with small steps. Even if you only have an extra $100 per month to save, allocating that cash wisely can help change your money mindset and develop good habits that will stay with you as your income grows.

Gabrielle Olya contributed reportage for this article.

More From GOBankingRates

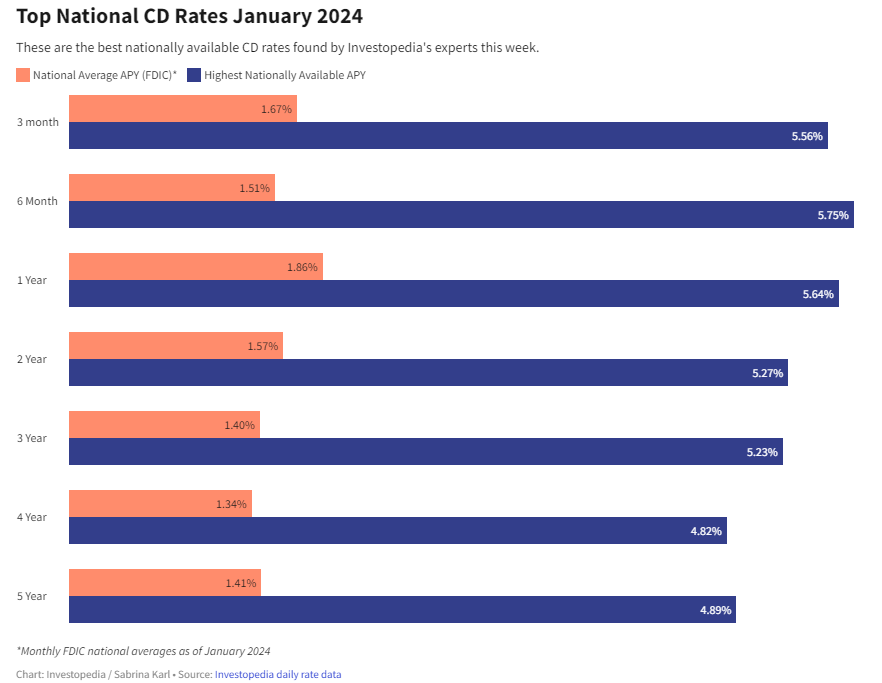

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create

What is the National Debt?

As a professional in the field of finance and economics, it is essential to have a comprehensive understanding of the national debt. The national debt refers to the total amount of money that a country owes to its creditors, which may include individuals, businesses, and other countries. In this art

How to retire in other countries? What are the best countries to retire abroad?

Retiring abroad has become an increasingly popular option for many people seeking a change of pace and a more affordable lifestyle. However, making the decision to retire in another country requires careful consideration and planning. In this article, we will explore the best countries to retire abr